Job Costing for Commercial Cleaning: Why Profitability Is Hard to Track (And How to Fix It)

How Modern Janitorial Software Enables Real-Time Profitability

A mid-sized BSC running $10M in revenue with just 5% labor overages loses $350K annually, often without knowing which accounts are responsible. This isn't a rounding error. It's the difference between growth capital and crisis mode.

Job costing should answer three basic questions: Is this account making money? Which sites need immediate attention? Is the contract priced for profitability? Most commercial cleaning companies struggle to answer these questions until weeks after the work is done. The problem isn’t mathematical—it's structural.

Even teams using time tracking apps, inspection software, or standalone payroll systems still struggle because the data lives in disconnected tools. Labor costs flow through one system, supply invoices through another, and payroll taxes get applied only after books close.

This fragmentation makes it hard to track cleaning company labor costs accurately, maintain reliable janitorial budget vs actual tracking, or catch problems while there's still time to correct them. Most operators discover overages only when payroll is processed, often weeks after the work happened. To understand how to fix it, we need to understand why job costing is uniquely challenging in janitorial operations.

What Job Costing Really Means in a Commercial Cleaning Business

At its core, job costing answers three questions:

- Is this account making money?

- Which sites need immediate attention?

- Is the contract priced for profitability?

To answer these reliably, every cost must tie back to the job: labor costs (the largest expense and biggest driver of variance), supplies and consumables (liners, chemicals, paper products, PPE), equipment and tools (shared assets that often distort "true cost"), and overhead allocations (supervision, inspections, travel time, admin load).

On paper, these categories are straightforward. In practice, accurate job costing depends on how well your janitorial software connects field work to payroll and the general ledger. When systems don't connect, job costing becomes more guesswork than analysis. That's why the question, 'do we make money on that building?' often requires pulling multiple reports instead of a quick dashboard check.

Why Job Costing in Janitorial Is Hard

Here's why accurate job costing is so challenging in janitorial:

1. The Labor Data Disconnect

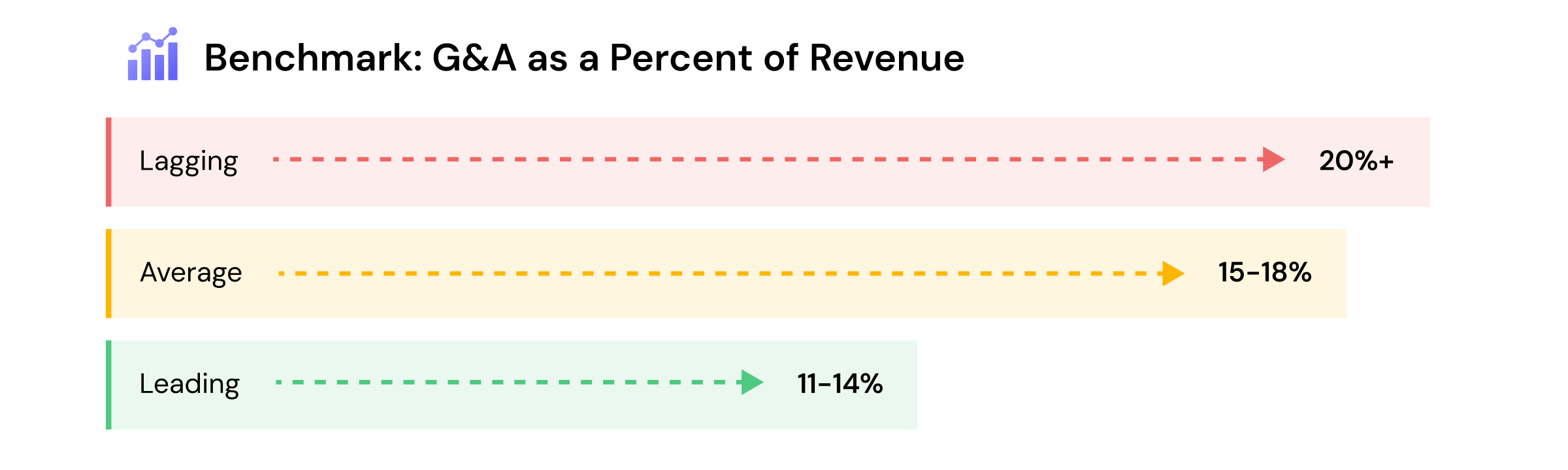

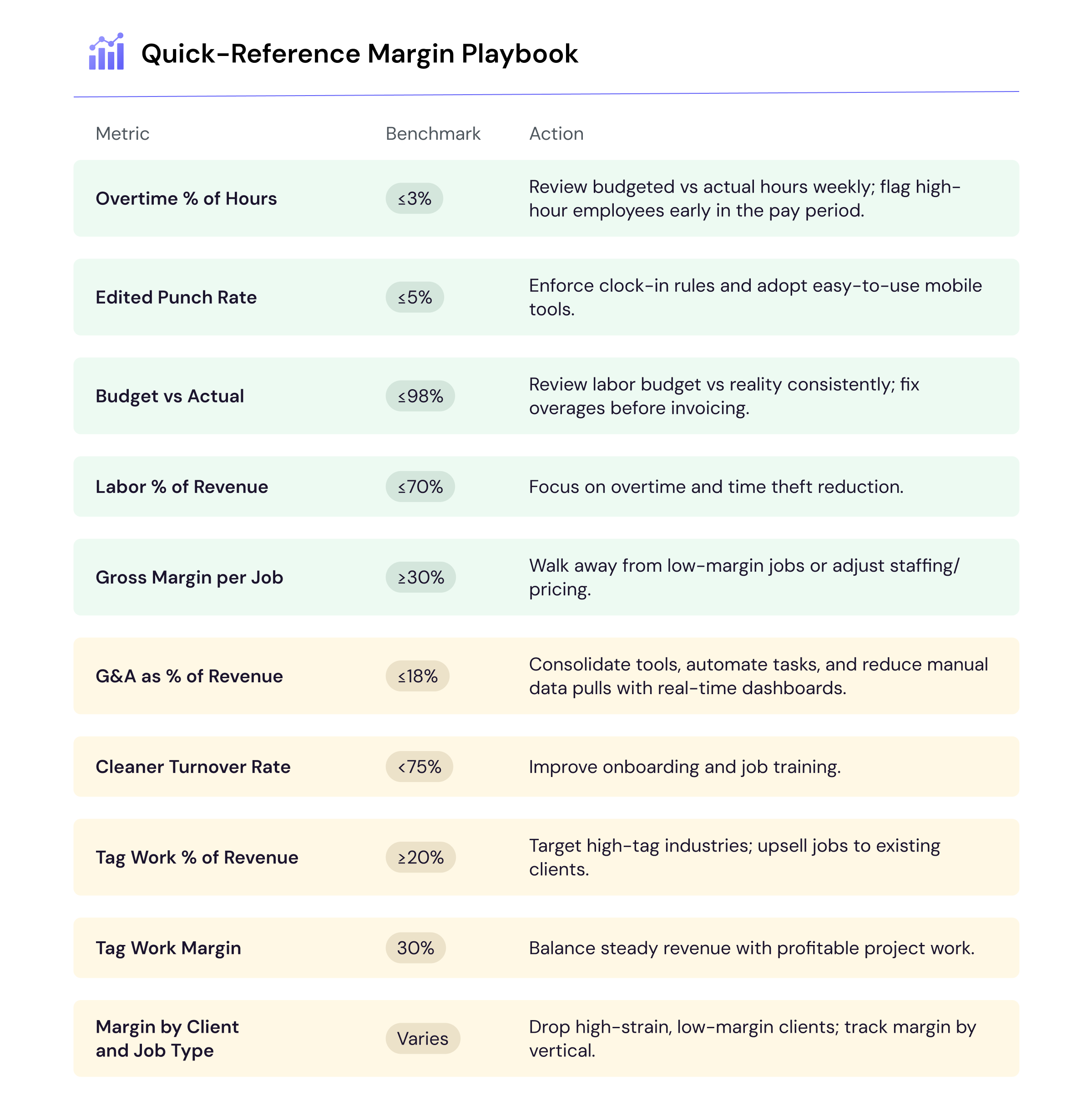

Labor is the foundation of job costing, and the most fragmented cost category in a cleaning company's P&L. Most BSCs aim to keep labor as a percentage of revenue below 70%. But without real-time visibility, overruns are discovered too late.

Labor data is broken into silos: hours come from scheduling systems, attendance is captured through mobile apps, overtime rules and union policies come from payroll, employer taxes and accruals may be applied after payroll closes, and actual labor cost is recorded only when accounting books the payroll run. These silos make it extremely difficult to track cleaning company labor costs in real time, or maintain accurate janitorial budget vs actual tracking by job.

2. Supply Costs Without Job Codes

Every commercial cleaning company receives large invoices from supply vendors. None of them include job codes. As a result, operators split invoices across accounts, supervisors guess which building used which items, bulk orders mask usage drift, and overconsumption remains invisible. Without intentional tracking, or without integrated systems, supply cost per job becomes an approximation instead of a measurement.

3. Equipment's Hidden Margin Impact

Most equipment isn't costed at the job level: vacuums rotate between buildings, autoscrubbers move with supervisors, and pads, cords, and parts are used inconsistently. This creates margin distortion because heavy-use buildings quietly burn through equipment, routing inefficiencies multiply wear, and supervisory practices influence lifespan. Few operators analyze equipment-driven variance, even though it materially affects long-term profitability.

4. The Overhead Allocation Gap

This is one of the most overlooked challenges in job costing. Operators inconsistently allocate supervision, inspections and QA time, travel between buildings, administrative load, issue resolution, and non-billable labor. Some use a flat percentage. Some ignore overhead altogether. Some apply it only once per year. This results in job margins that appear healthy but collapse when overhead hits the books.

The Practical Reality: Most "Job Costing" Isn't Actually Job Costing

Because the data is fragmented, most companies rely on a quick look at labor hours, a rough estimate of supply usage, broad overhead percentages, supervisor intuition, and lagging payroll data. Without connected data, job costing requires exporting spreadsheets, re-entering data, reconciliation between systems, reviewing invoices with hundreds of line items, and fixing timesheets manually. This approach makes it nearly impossible to manage proactively. Budget tracking becomes a monthly postmortem instead of a weekly operational tool.

Why Accurate Job Costing Matters More Than Ever

Comprehensive job costing is one of the strongest competitive advantages in the janitorial industry. It gives operators clarity around which accounts generate true contribution margin, where labor overruns are occurring, where overtime exposure is building before payroll closes, how supply usage compares to scope-of-work, whether supervision load aligns with contract value, which supervisors run high-efficiency operations, and which buildings consistently run over budget.

Proactive Labor Management

When job costing shifts from a month-end accounting exercise to a weekly operational practice, everything changes. Margins become predictable, overages are corrected early, labor efficiency improves, supervisors manage proactively, and clients trust the results. This is the future of commercial cleaning operations: connected, continuous margin intelligence driven by modern systems and operational discipline.

From Reactive to Proactive: The Path Forward

The next generation of profitable BSCs and commercial cleaning firms will operate with unified data: schedules, attendance, inspections, payroll, AP, and job-level costing flowing together. Job costing isn't just a finance workflow. It's becoming the operating system of the entire business.

The most profitable operators aren't necessarily running the most expensive systems, they're running the most connected ones. They know by Tuesday (not month-end) which accounts are heading off budget.

What Real-Time Job Costing Looks Like

When operations, payroll, and accounting connect in one system, every shift flows into payroll, every payroll run posts to job costs, and every dollar ties back to the account that caused it. Budget variance is visible daily, not monthly. Labor cost per job updates automatically. Margin protection becomes proactive, not reactive. This is the promise of modern commercial cleaning software: not just better tools, but better economics.

Take Action

Download the Janitorial Margin Playbook to see where your margins stand and which metrics matter most.

See how BrightGo connects operations to accounting in one system built for commercial cleaning contractors.

_1_11zon.webp)